Way too many People in the us have trouble with debt. A survey conducted because of the Hometap inside the 2019 away from almost 700 U.S. homeowners indicated that although homeowners is actually household-rich, also dollars-terrible, with little date-to-day exchangeability. Survey takers indicated whenever they did has actually https://paydayloansalaska.net/newhalen/ loans-free accessibility its house’s collateral, for example a property security progress, they’d use it to settle credit debt, medical bills, or even assist friends pay off obligations.

Of several people replied which they have not actually thought possibilities to help you make use of their house security. In a nutshell, they feel trapped as the available monetary selection only apparently include more obligations and you may attract with the homeowner’s monthly equilibrium sheets. There is also the difficulty regarding qualification and you can recognition, because it’s tough to meet the requirements of a lot resource possibilities, such as a home collateral financing, which have poor credit.

The good news? That it domestic rich, cash bad position quo does not have any to continue. Here, you’ll find out concerning the significance of borrowing, as well as how you might however accessibility your house security if your very own is sub-standard.

What’s Borrowing and why Does it Number to Loan providers?

Borrowing from the bank is the capacity to to borrow money, see points, otherwise fool around with properties when you’re agreeing to incorporate payment at the a later on big date. The phrase credit rating describes good around three-thumb count that indicates the level of trustworthiness you presented when you look at the for the last owing to knowledge of loan providers, lenders – essentially, any business who has got provided you currency. This information is achieved inside a credit history due to a choice of various present, like the number of handmade cards you have, plus any an excellent stability on them, their reputation for finance and you may payment conclusion, timeliness regarding invoice payment, and you may extreme trouble such as for example bankruptcies and foreclosure.

Put differently, lenders wish to be due to the fact sure you could which you can shell out straight back any money they offer for you, and you will checking your own borrowing from the bank is an easy and you can relatively comprehensive means to get this information.

While carrying many loans and are also worried about the borrowing from the bank, it might seem that family collateral is inaccessible. However with an alternate, non-loans resource choice available to a number of property owners, you might be surprised at what you could accessibility. Listed below are some ways you can make use of your home equity to begin with playing with that liquidity to arrive your financial desires. ?

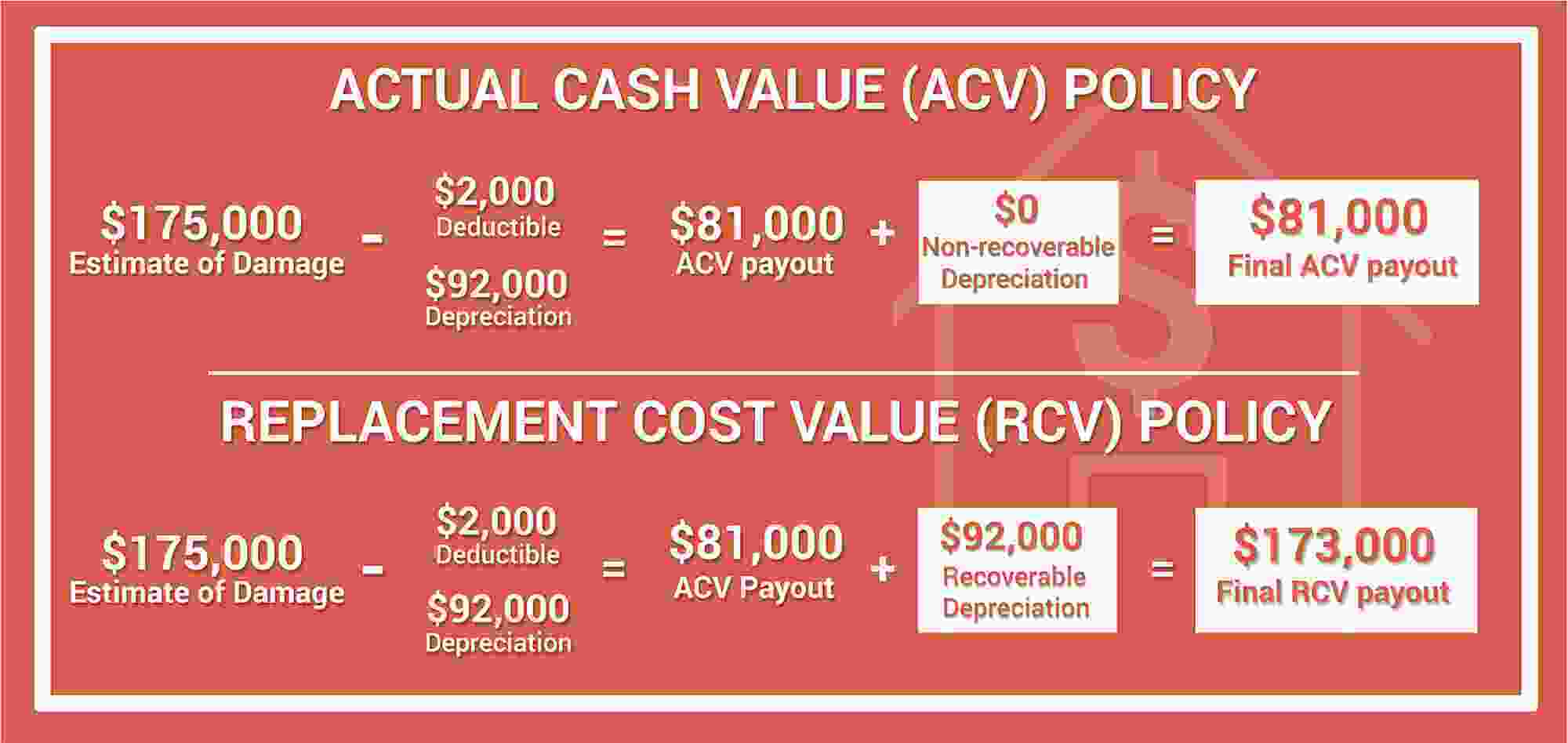

Comprehend the graph less than for an easy article on the options that might be available according to your credit rating, then read on for more within the-depth definitions of any.

Cash-Aside Refinance

A funds-aside re-finance is when you, the latest homeowner, take-out yet another, large mortgage, pay back your current mortgage, and make use of the excess to fund your circumstances. This can be done throughout your present bank or another type of bank that is maybe not noticed an additional mortgage. Centered on Bankrate , your typically you prefer at least 20% equity in your assets so you’re able to qualify, and you will pay desire on life of the borrowed funds (usually fifteen or thirty years). By the much time time of a cash-aside refi (since the these include commonly known), you will need to ensure the interest rate and your requested fees bundle match your month-to-month finances. Homeowners are typically necessary to provides a credit rating minimum of 620 as acknowledged to possess a cash-aside re-finance.

Household Guarantee Financing or House Equity Line of credit

Are you willing to be eligible for a home equity loan otherwise a property security line of credit (HELOC) with bad credit? Basic, you need to know the essential difference between these household security solutions.

Property collateral financing allows you to borrow money with the security of your home due to the fact guarantee. Good HELOC, likewise, functions similar to credit cards, in the same way that you can mark funds on a concerning-needed basis. Having both home collateral finance and you will HELOCs, your credit score and you can family guarantee value will have a part in how much you are able to use plus desire rate.

The minimum credit history you’ll need for property collateral mortgage and you can a beneficial HELOC are often no less than 620, though it hinges on the lending company. However, even if you try not to satisfy it minimum credit score getting a property collateral loan otherwise HELOC, avoid being annoyed. Julia Ingall with Investopedia claims residents having less than perfect credit is to research buy loan providers available to working with individuals instance him or her. In addition, Ingall notes one handling a mortgage broker helps you see your alternatives and support credible loan providers.

Home Collateral Improve

Property guarantee improve offers people the ability to utilize the long term property value their home so you’re able to availability the collateral today. A property security money are a smart way to do merely one.

At the Hometap, residents can also be found household collateral investment so they can fool around with a few of the equity obtained obtained in their house accomplish most other monetary desires . Brand new homeowner gets dollars without having to promote or take away a loan; as there are no appeal without payment. . Another advantage from a Hometap Funding is that numerous products is taken into consideration to approve a candidate – credit history is not the determining standards.

Promote Your home

For the majority, its a last lodge, but residents having poor credit have access to the residence’s equity of the promoting it downright. Obviously, that it decision is predicated abreast of selecting a cheaper domestic to have your next domestic, in addition to positive mortgage terms and conditions for your brand new place, and ensuring that you don’t spend excessively with the a property charge or moving can cost you. You additionally could possibly replace your credit score ahead of you reach this point. Overseeing your credit score to save an eye aside having possible disputes and discrepancies, keeping an equilibrium really below your borrowing limit, and you will remaining dated membership discover are common good metropolises to begin with.

When you find yourself effect home-rich and cash-bad instance way too many People in america , you’ve got a number of choices to supply your residence guarantee. Just like any biggest financial support choice, consult with a dependable financial professional to choose the best direction away from action, and also moving with the your aims.

I perform all of our best to make sure what when you look at the this post is just like the real to as of new day its had written, but anything change easily either. Hometap doesn’t promote or display people linked other sites. Individual things differ, very consult your very own finance, taxation or legal professional to determine what makes sense for your requirements.